ESG & Institutional Investment

Part 4

Henrique C. Martins

SASB

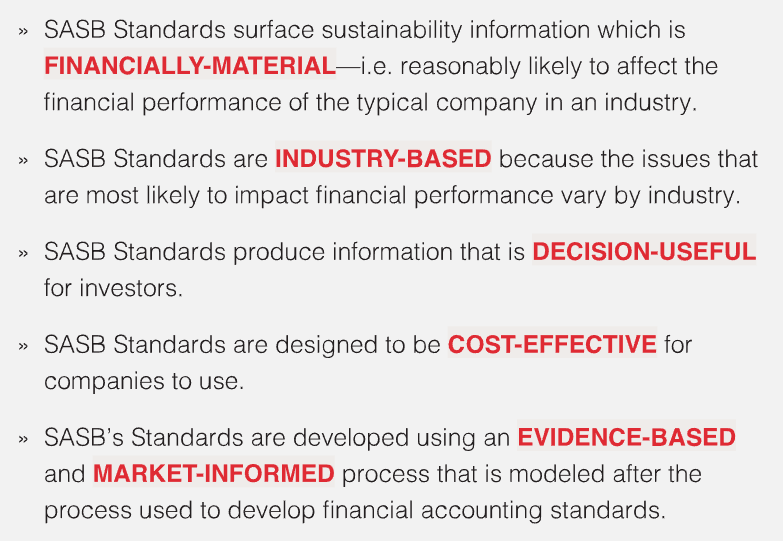

SASB Standards guide the disclosure of financially material sustainability information by companies to their investors.

Available for 77 industries, the Standards identify the subset of environmental, social, and governance issues most relevant to financial performance in each industry.

SASB was founded as a nonprofit organization in 2011.

The big word here is materiality.

- Remember, ESG issues are industry-specific. So what is important for one industry might not be for another.

- SASB creates a framework to understand and anticipate what is materials to industries.

SASB

The goal is to address the gap between traditional financial statements and the sustainability factors that can affect firm’s long-term value.

Material factor:

Has a real and profound impact on the firm’s valuation, operations, strategy, etc.

For the purpose of SASB’s standard-setting process, information is financially material if omitting, misstating, or obscuring it could reasonably be expected to influence investment or lending decisions that users make on the basis of their assessments of short-, medium-, and long-term financial performance and enterprise value. (Source)

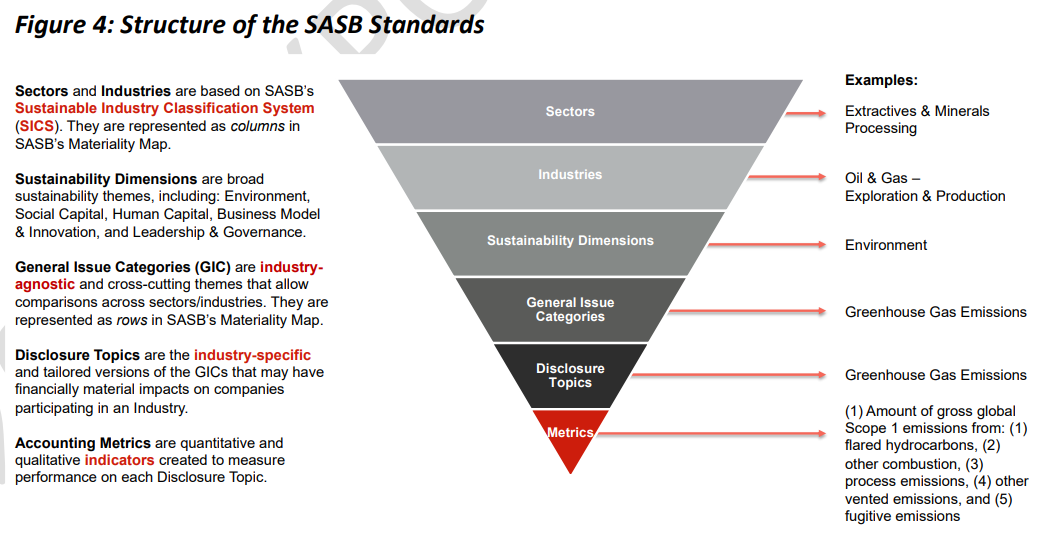

SASB

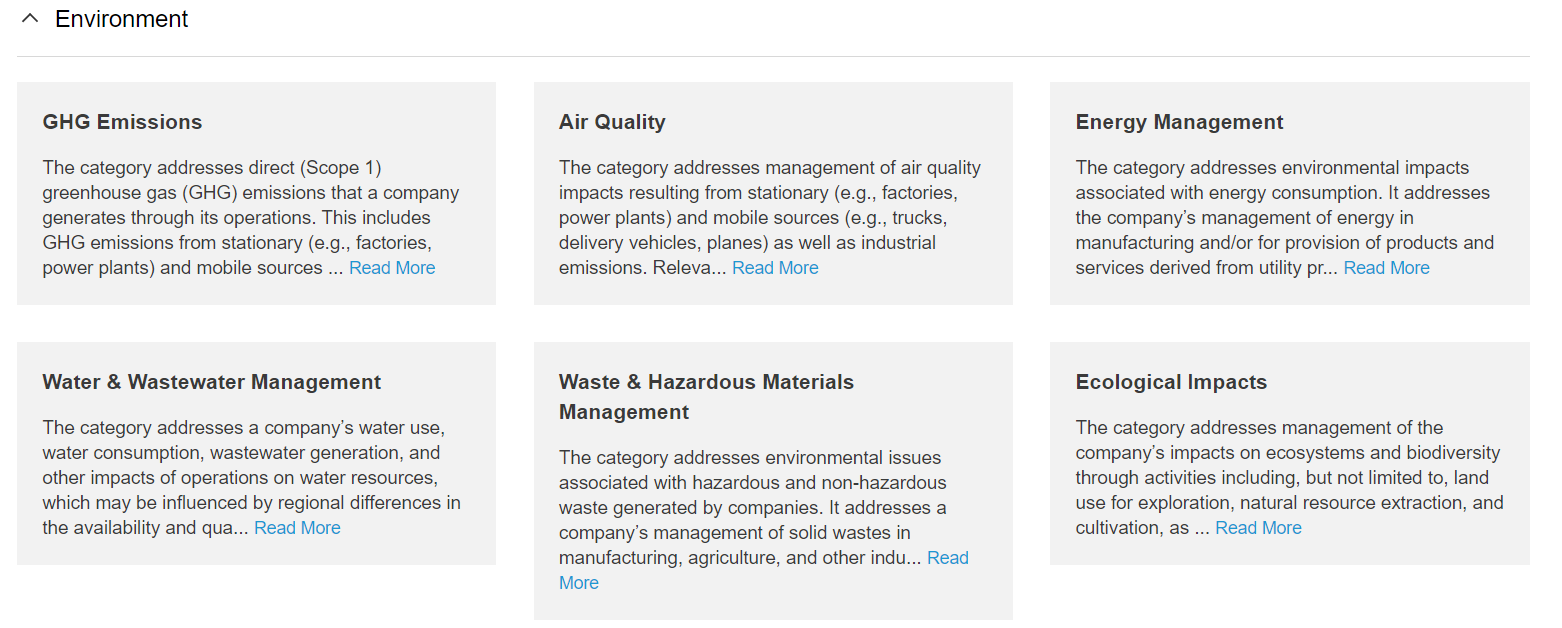

Five dimensions:

- Environment

- Social Capital

- Human Capital

- Business Model & Innovation

- Leadership & Governance

Each dimension has several General Issue Categories. Total of 26 GICs.

Environment (Source)

Environment. This dimension addresses direct environmental impacts that are linked to a company’s ability to create value over time and are a result of activities which include natural resource extraction, land cultivation, product manufacturing, and the use of energy and water.

The impacts include greenhouse gas emissions, water consumption, waste generation, and biodiversity loss.

Environmental impacts arising out of the use of a company’s products and services are excluded from this sustainability dimension and are instead captured under the “Business Model and Innovation” dimension.

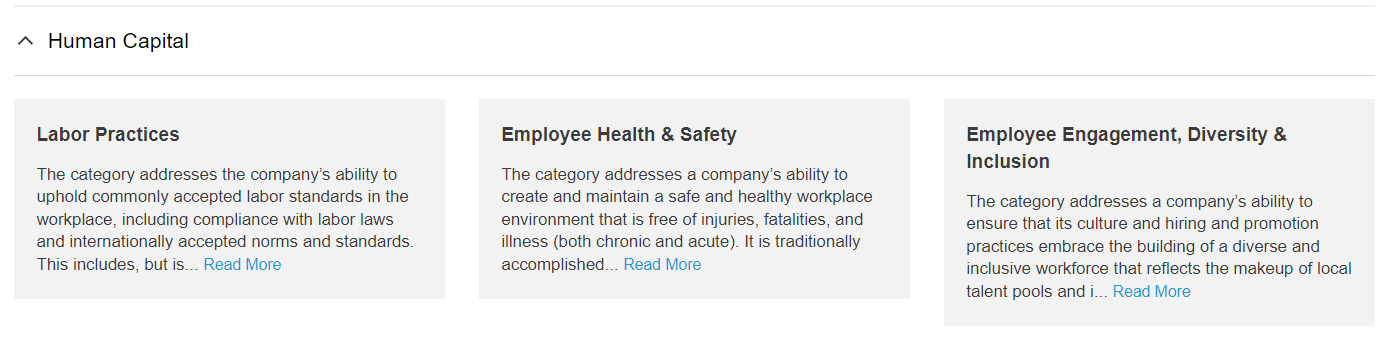

Human Capital (Source)

Human Capital. This dimension addresses issues that affect a company’s workforce, which is often a key resource to delivering long-term value.

It includes issues such as management of the health and safety of the workforce, labor practices, and the organizational culture.

This sustainability dimension addresses issues related to workforce engagement and the building of a diverse and inclusive workforce. These issues may affect the levels of workforce productivity, as well as the attraction and retention of members of the workforce in highly competitive or constrained markets for specific talent, skills, or education.

Business Model & Innovation (Source)

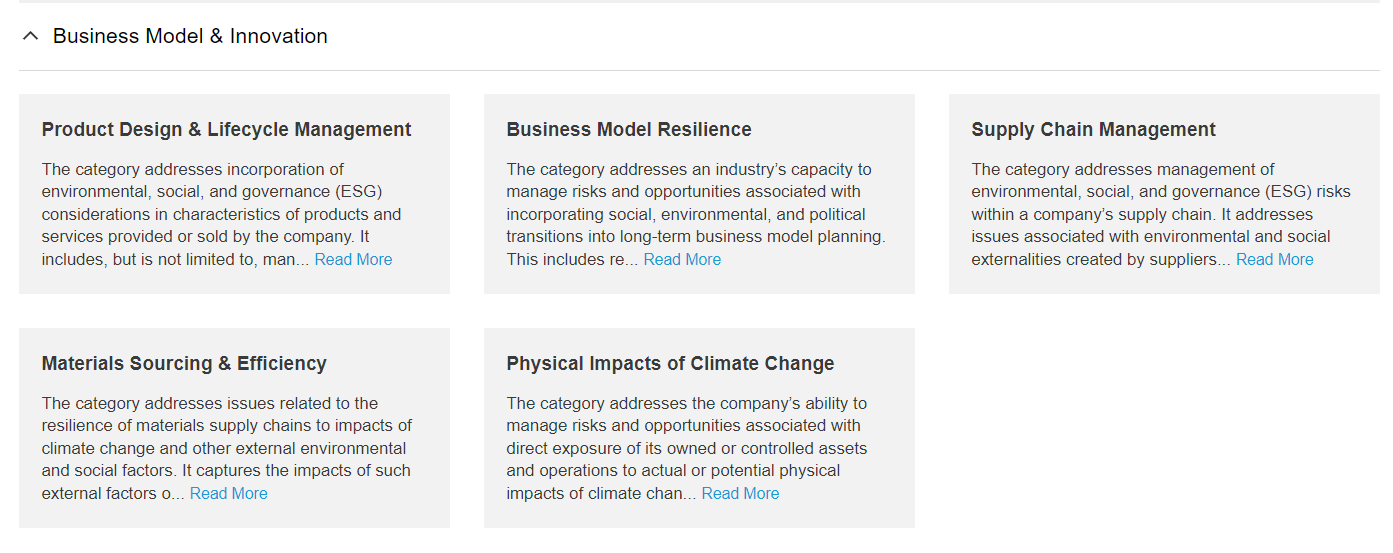

Business Model and Innovation. This dimension addresses the integration of environmental, human, and social issues in a company’s value-creation process.

This includes business model resilience and the manner in which a company integrates sustainability considerations into the development, production, and sales of products or services. The dimension includes the design and innovation of products and services, including the impacts of such products in the use phase and those stemming from product disposal.

Furthermore, the dimension includes the extent of a business model’s integration of physical impacts of climate change on assets availability and pricing of key resources, and impacts of supply chains.

Although this sustainability dimension is centered on the integration of sustainability into the company’s business model, including the indirect impact of the company’s products and services, the environmental, social, and human capital impacts that are directly generated by the company’s operations are captured under the “Environment,” “Social Capital,” and “Human Capital” dimensions, respectively.

Leadership & Governance (Source)

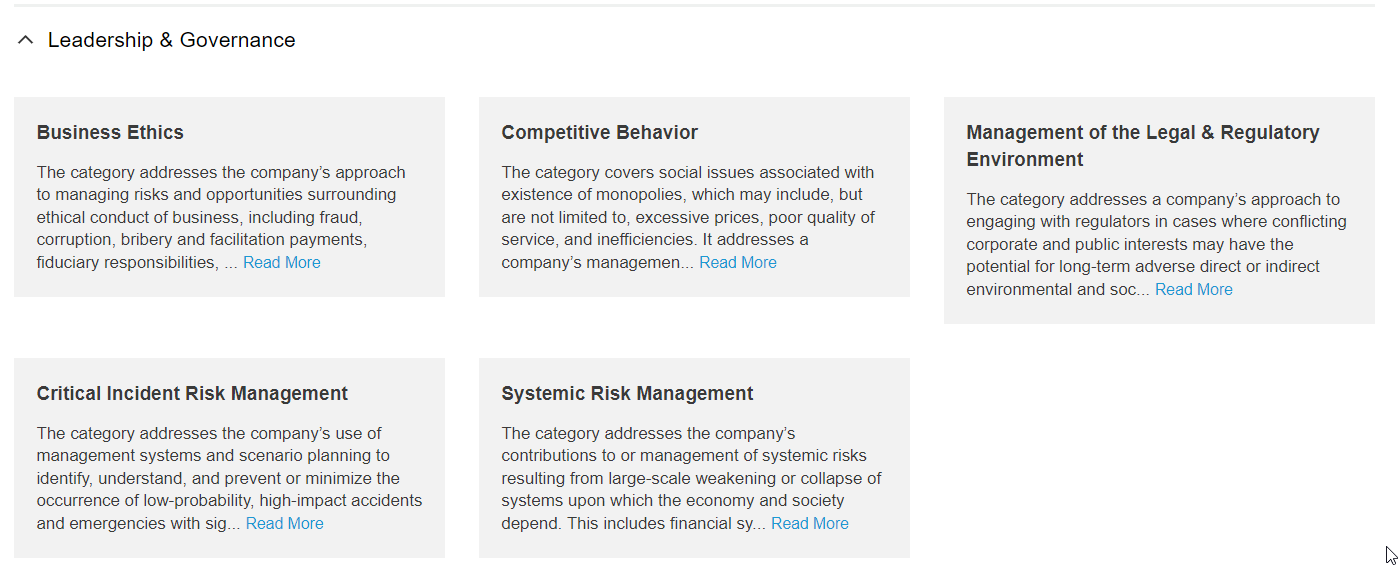

Leadership and Governance. This dimension involves the governance and management of key industry issues that may create conflicts with the interests of broader stakeholder groups, and therefore may lead to liabilities or impacts on a license to operate.

The dimension includes conducting business activities in compliance with industry laws and regulations, and in accordance with the industry’s leading standards of professional integrity.

Issues captured in this dimension include, anticompetitive practices, ethical conduct of business, and engagement with regulators on environmental, social, and human impacts. This dimension also addresses the management of risks related to low-probability, high-impact accidents and emergencies that generate a multitude of sustainability impacts.

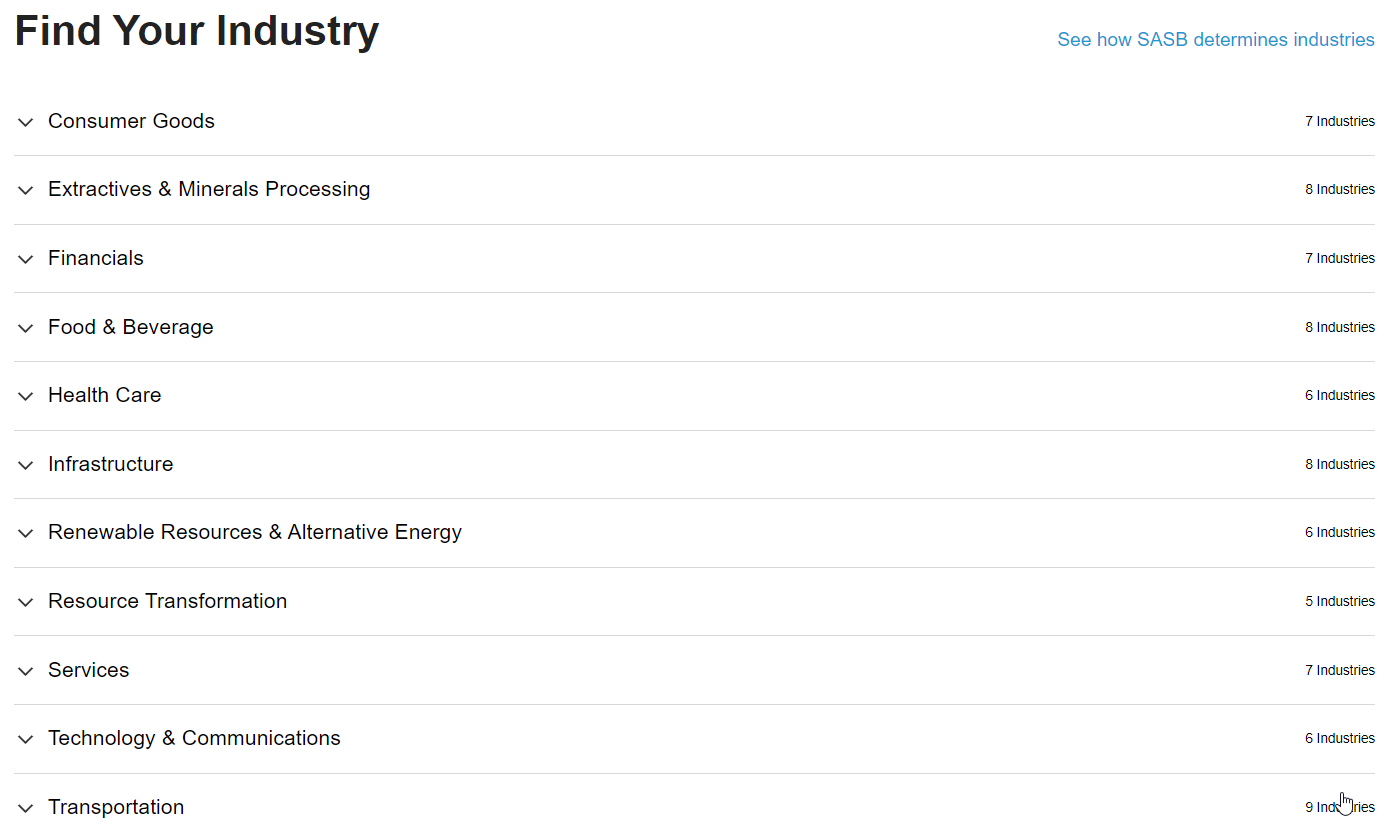

Industries definition

After defining the Dimensions, you need to define an industry classification: SICS

Most major industry classification systems use sources of revenue as the basis.

In order to group like companies based on their sustainability-related risks and opportunities, a new industry classification was needed. The Sustainable Industry Classification System® (SICS®) solves that problem.

The differences between SICS® and traditional industry classification systems can be categorized in three types: (1) new thematic sectors; (2) new industries with unique sustainability profiles; and (3) industries classified in different sectors.

Industries definition

After defining the Dimensions, you need to define an industry classification: SICS

Unlike other industry classification systems—which use common financial and market characteristics— SICS® uses sustainability profiles to group similar companies within industries and sectors.

In SICS®, a company’s sustainability risks and opportunities are more important for its classification than other traditional factors, such as economic cycles and revenue streams. A company’s SICS® classification is determined by overlaying its sustainability framework to other industry taxonomies.

Industries definition

After defining the Dimensions, you need to define an industry classification: SICS

SASB contains 77 industries.

For context: https://siccode.com/

- There is more than one layer of classification.

Industries definition

SICS (source)

SASB

Dimensions (5): check.

Industries classification (77): check.

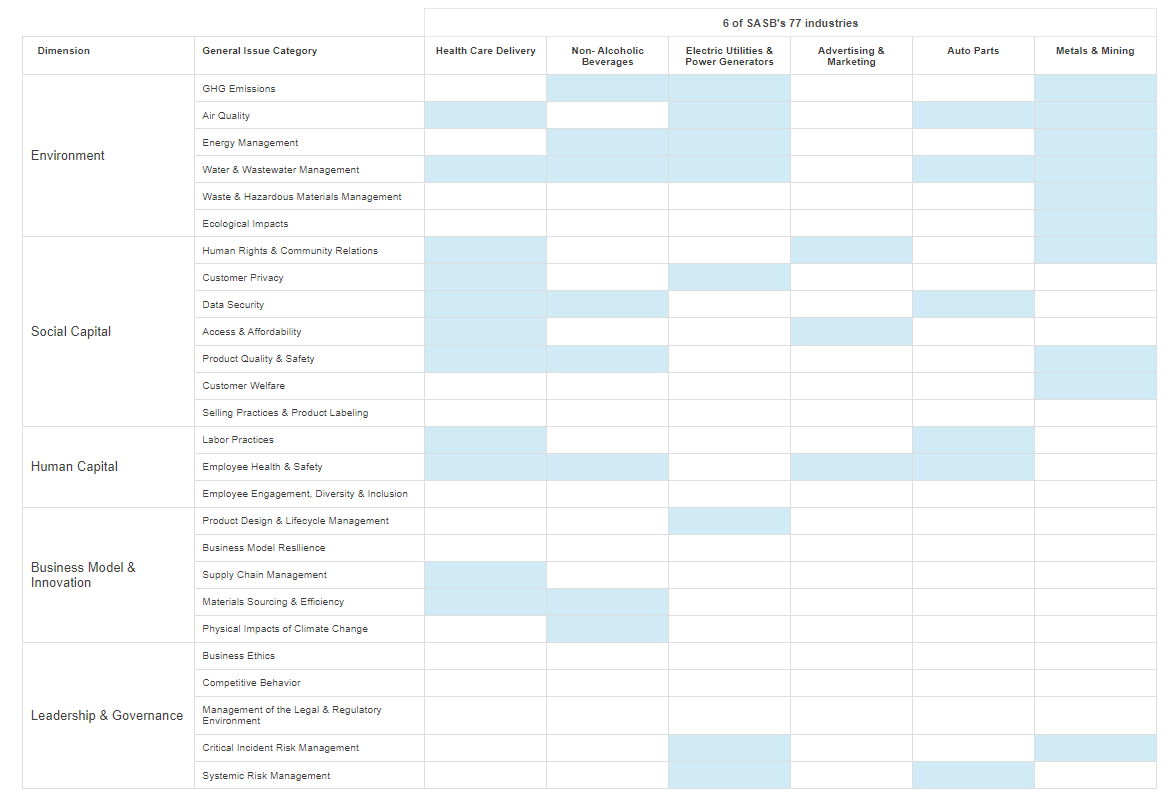

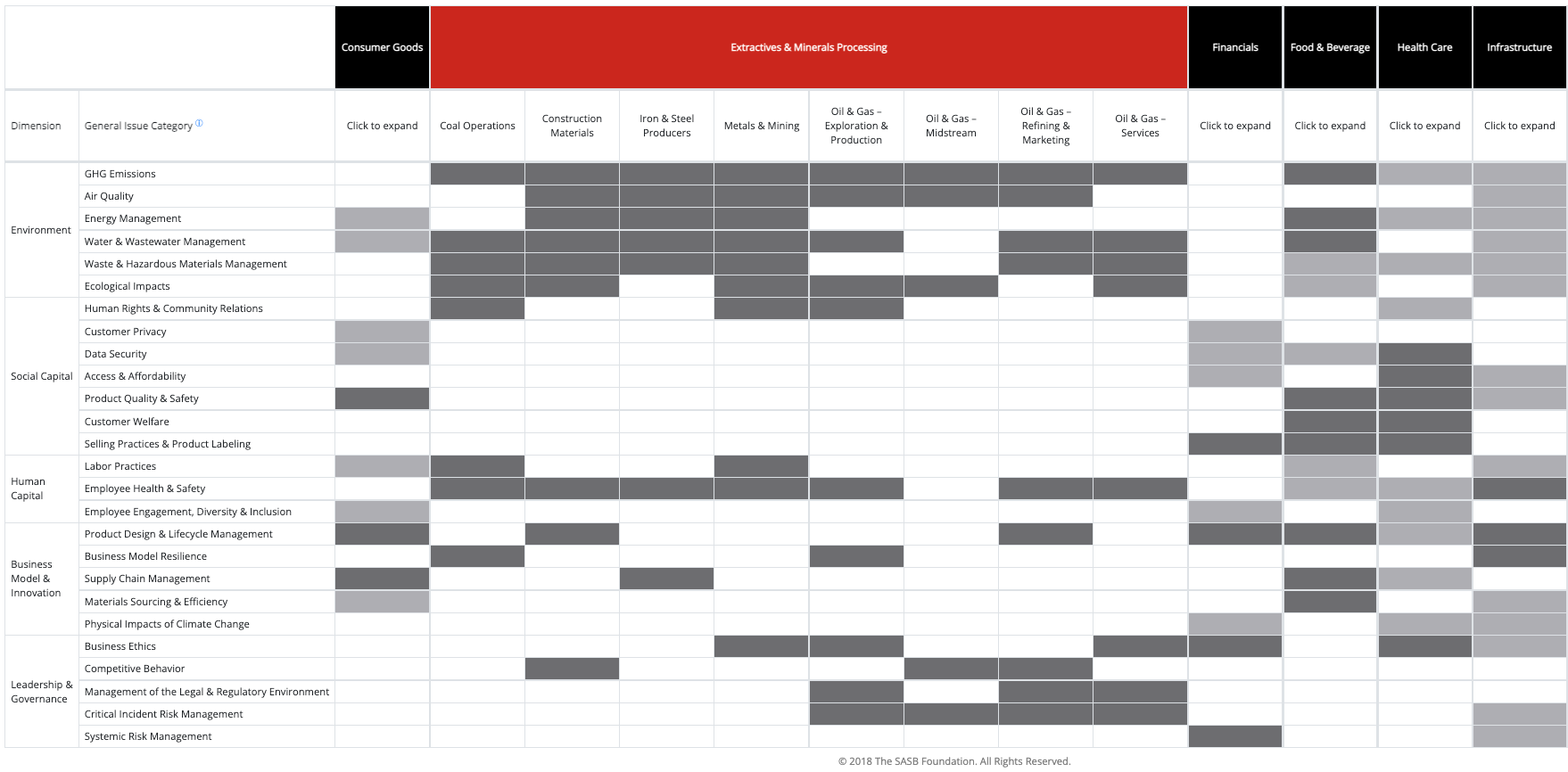

The next step is to create a matrix showing which issue is material to each industry.

- There are 26 general sustainability issues (GICs),

Blue squares contain material issues.

Materiality Map

Businesses can use the map to pinpoint, manage, and report on the disclosure topics most relevant to their industry, along with the associated accounting metrics.

Investors use to assess the metrics and overall firms’ sustainability performance.

See Metals & Mining Sustainability Disclosure topics & Accounting Metrics (Source)

In class activity

In pairs, select one company of your choice.

Find the Relevant issues of each dimension.

Write one paragraph with your comments about the issues.

- Do you agree or not agree?

- Is something missing?

- What is your overall perception about the issues?

This activity will substitute a Quiz.

I hope you like this class!

Find me at:

https://eaesp.fgv.br/en/people/henrique-castro-martins

https://www.linkedin.com/in/henriquecastror/

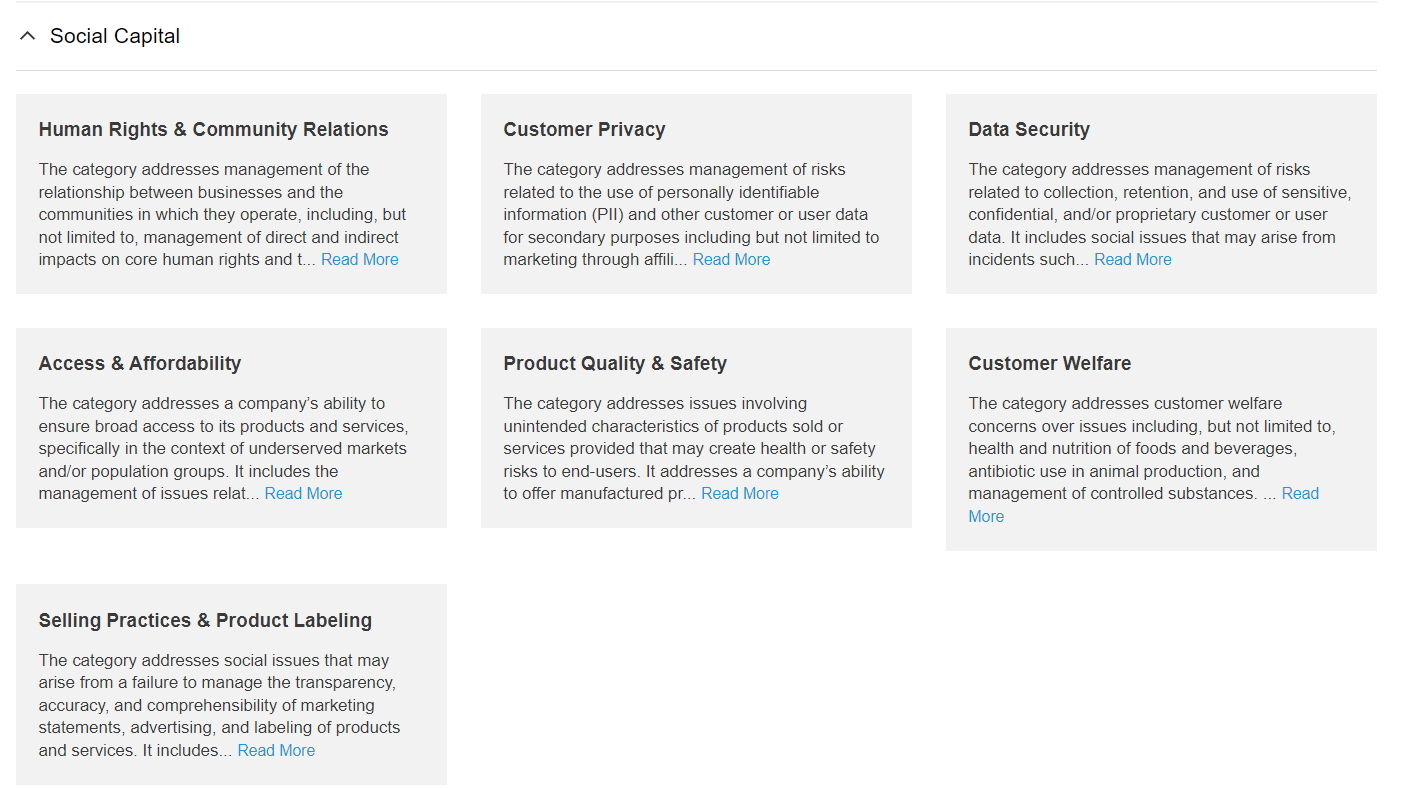

Social Capital (Source)

Social Capital. This dimension addresses a company’s impact on external stakeholders and the management of those stakeholder relationships, including a company’s license to operate. External stakeholders include customers, local communities, regulators, and the public.

Impacts on these stakeholders may relate to issues such as human rights, protection of vulnerable groups, local economic development, access to and quality of products and services, affordability, responsible business practices in marketing, and customer privacy.

Stakeholders that are directly or indirectly employed by the company are excluded from this sustainability dimension and are instead captured under the “Human Capital” and/or “Business Model & Innovation” dimensions.