ESG & Institutional Investment

Part 3

Henrique C. Martins

Institutional Investment

Traditionally, investment theory has focused on how investors should allocate capital to achieve the highest possible financial returns, subject to managing risk (i.e., the return-risk optimization or the Sharpe ratio optimization).

Similarly, those seeking to deploy resources to obtain social goals focused on philanthropy, non-profit management, and cost-benefit analyses.

However, some years ago, individuals and institutions recognized that investment decisions themselves may further (or hinder) the achievement of social goals.

- For instance: in the 80s, 500+ Billion divested from South Africa in protest against Apartheid.

- This type of practice still occurs to date.

Institutional Investment

Institutional investors are those that do most of these practices.

They play a central role in modern capital markets.

Examples of institutional investors

- Banks and financial institutions

- Pension funds

- Insurance companies

- Hedge funds and mutual funds

- Sovereign wealth funds

- Venture capital funds

Institutional Investment

Institutional investors usually:

- Manage large sums of money

- Buy large positions

- Some can trade frequently

- Have infrastructure to affect companies

- Have knowledge

- Buy diversified portfolios

Institutional Investment

Institutional investors play a significant role in modern Capital Markets

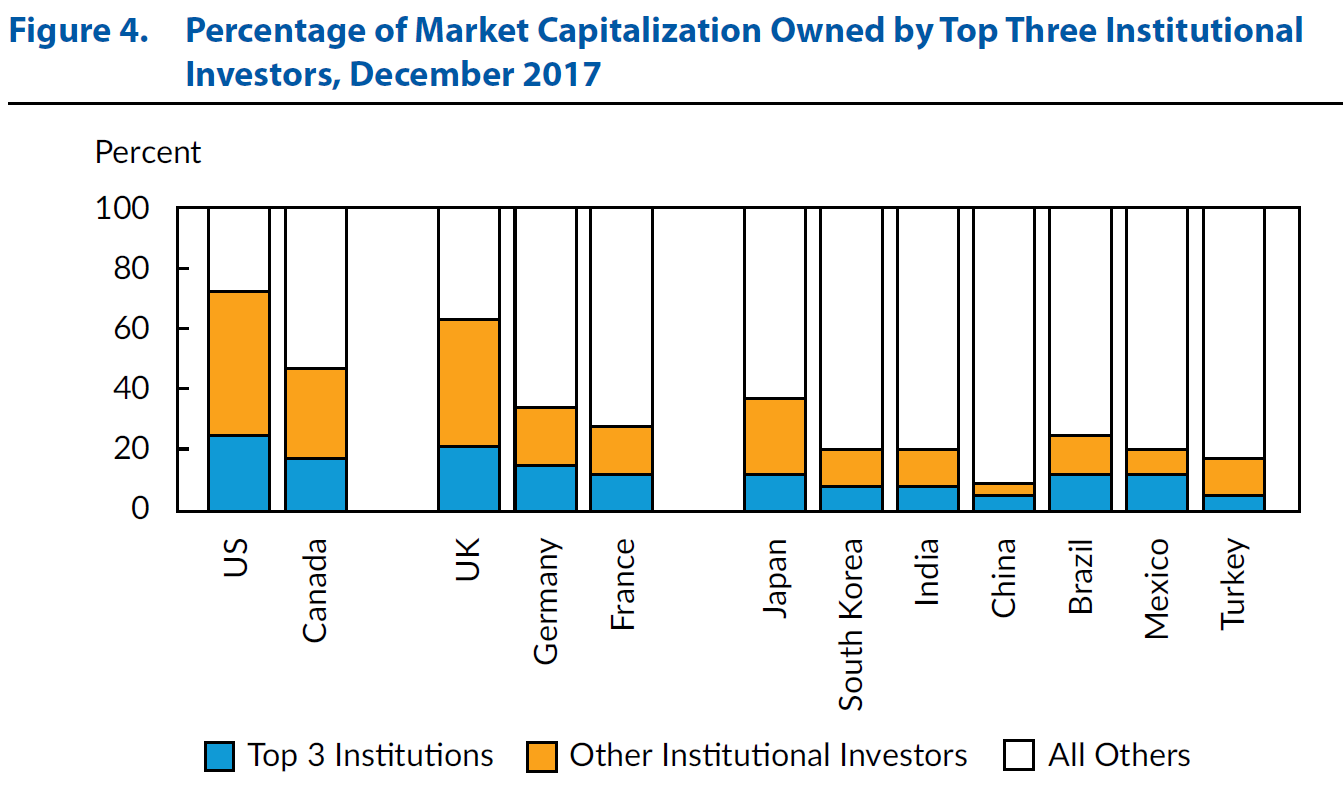

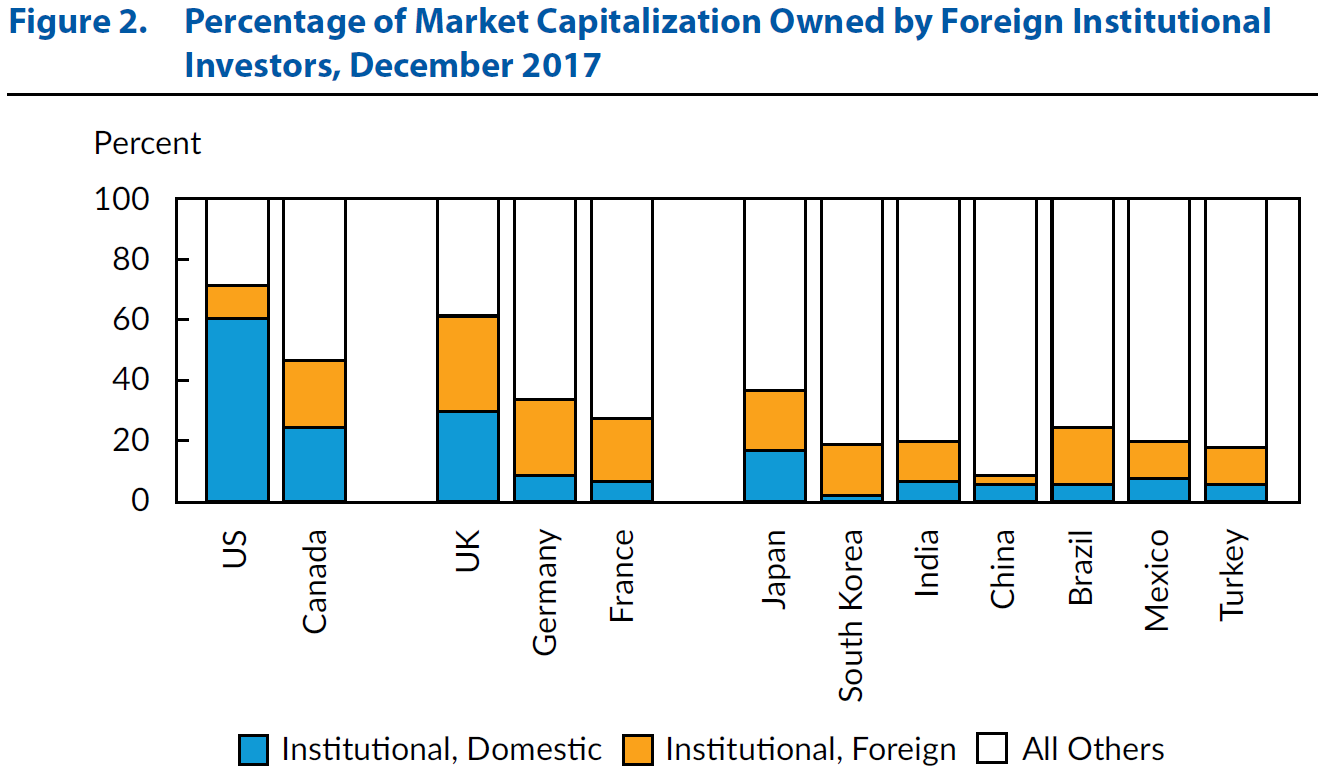

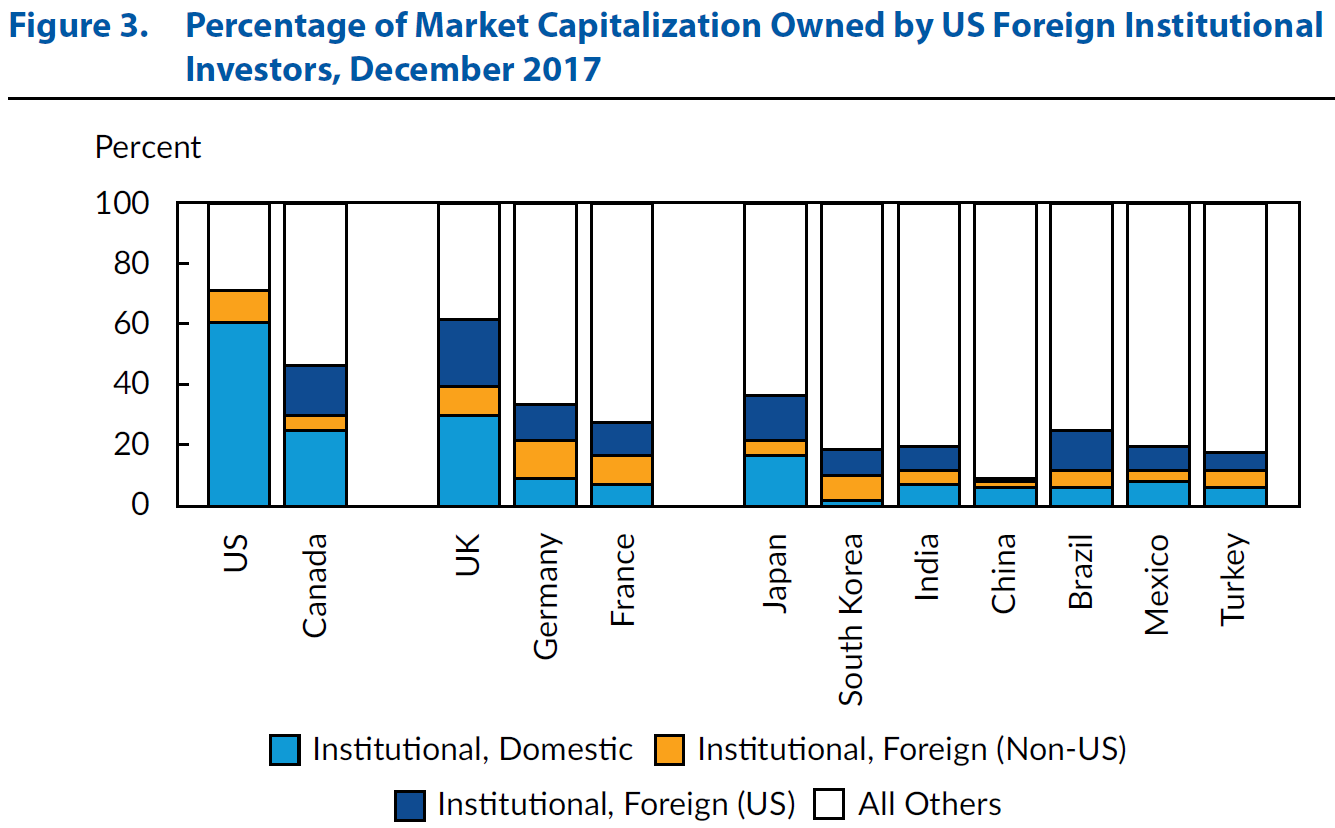

Institutional Investment

Foreign institutional investors are a thing in some countries.

Institutional Investment

Foreign institutional investors are a thing in some countries.

The role of institutional investors

Institutional investors usually:

- Select directors

- Can impact practices

- “Vote” mechanism

- Have power to persuade management

- “Walk away” mechanism

- Have connections to other firms

- “Supply chain” mechanism

The role of institutional investors

Therefore, they are well placed to interfere in the management of modern corporations

Institutional Investment

Classical finance theory suggests a simple but powerful framework for asset allocation:

- investors need only hold two assets—a risk-free bond, and a market portfolio.

- The ratio of these assets should depend on an individual’s risk appetite.

Advocates for sustainable investing argue that just as an individual’s public and private actions have positive and negative consequences on others, so too do the firms in which individuals invest. This introduces an additional dimension: social motivation.

Socially Neutral: seek return-risk optimization.

Socially Conscious: seek optimization, but uses ESG as constrain.

Socially Motivated: seek to impact the world by social and environmental change.

The role of institutional investors

Institutional Investment

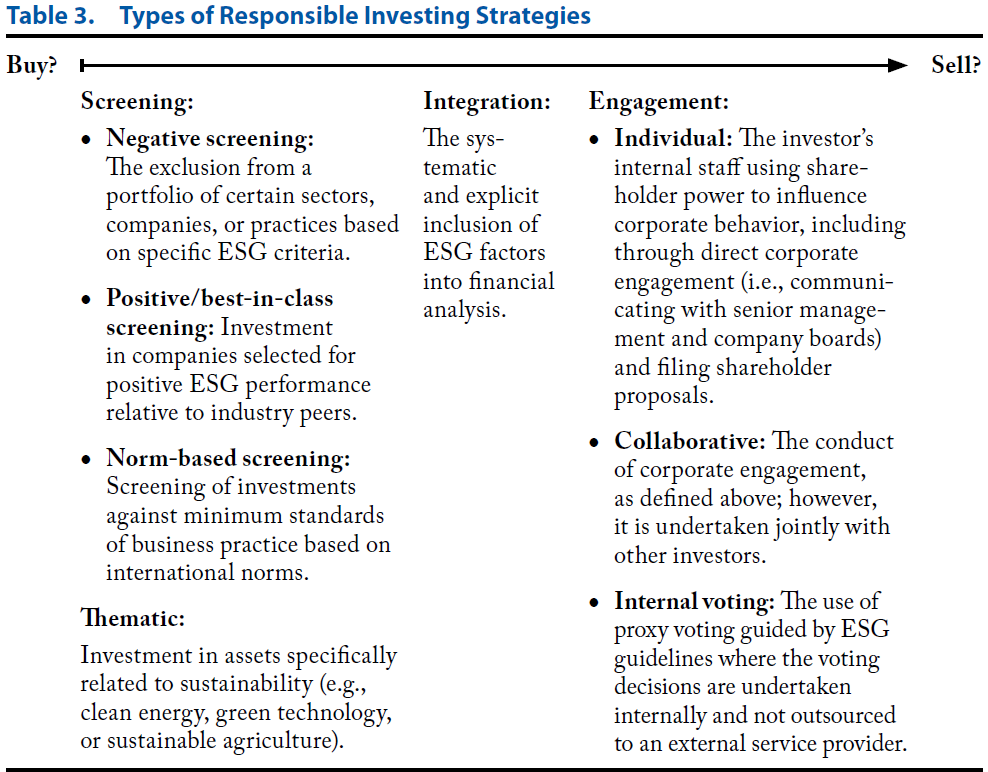

In order to “affect” management, institutional investors have some strategies today.

- Negative screening

- Positive (best-in-class) screening

- Norm-based screening

- Thematic

- Integration

- Individual engagement

- Collaborative engagement

- Internal voting

Negative Screening

The largest and arguably best-known variation of sustainable investing is screening—including or excluding certain sectors or companies based on specific non-financial criteria.

Negative screening is the idea that an institutional investor will not invest in particular industries or companies.

Negative screening is the the exclusion from a portfolio of certain sectors, companies, or practices based on specific ESG criteria.

The most longstanding strategy is negative screening, which—based on moral, norm-based, or ethical considerations—excludes stocks with worse ESG characteristics from a portfolio (Hong and Kacperczyk 2009).

Positive Screening

Investment in companies selected for positive ESG performance relative to industry peers.

The problem with this strategy is that you need to rely on a third-party ESG score to assess which companies to invest.

This is the investment in best-of-class companies.

Norm-based screening

Screening of investments against minimum standards of business practice based on international norms.

For instance, when the investor buys stock from a company that has signed the UN Global Compact Principles.

UN Principles

Human Rights

Principle 1: Businesses should support and respect the protection of internationally proclaimed human rights; and

Principle 2: make sure that they are not complicit in human rights abuses.

Labour

Principle 3: Businesses should uphold the freedom of association and the effective recognition of the right to collective bargaining;

Principle 4: the elimination of all forms of forced and compulsory labour;

Principle 5: the effective abolition of child labour; and

Principle 6: the elimination of discrimination in respect of employment and occupation.

UN Principles

Environment

Principle 7: Businesses should support a precautionary approach to environmental challenges;

Principle 8: undertake initiatives to promote greater environmental responsibility; and

Principle 9: encourage the development and diffusion of environmentally friendly technologies.

Anti-Corruption

- Principle 10: Businesses should work against corruption in all its forms, including extortion and bribery.

Thematic

Thematic investing consists of dedicated investment vehicles that allocate capital directly to sectors that are positioned to take advantage of certain ESG themes (e.g., renewable energy), and in fixed income, these include green bonds (which finance environmental projects) and social bonds (for social projects)

Integration

A second (and perhaps more comprehensive) strategy is integration, which consists of changing traditional investment processes to incorporate ESG data and insights into the overall evaluation of an investment.

In this approach, investment teams use sustainability data to create a more holistic view of investment risks and opportunities, regardless of whether the investment fund has a sustainable mandate.

It includes the ESG information during the research phase, security valuation, or portfolio construction—or later, during monitoring and risk management.

Personally, I don’t think there is an optimal strategy here. The industry is still building the protocol, in my view.

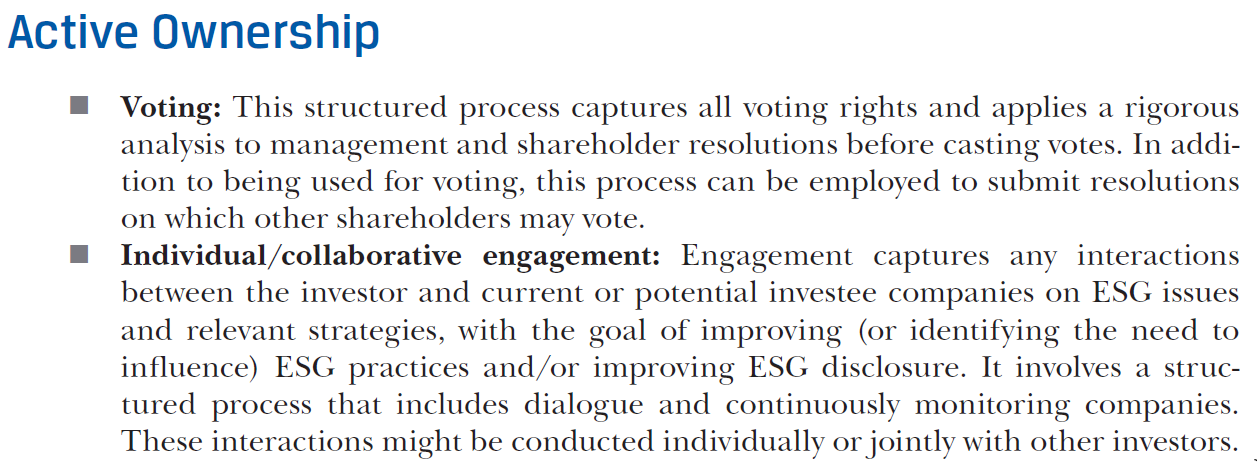

Engagement

The third type of strategies consists of engagement with corporate management and occurs subsequent to making an investment.

Through engagement (also known as active ownership or stewardship), investors can use their position as partial owners of companies to improve how those companies are managing or disclosing ESG performance.

Engagement involves discussing ESG issues with management (via private meetings or letters and dialogue during earnings calls or roadshows) or formally expressing approval or disapproval through the votes that their shareholdings entitle them to.

Investors can engage individually, in collaboration with other investors, or through an outsourced engagement service provider.

This is the main channel, in my view.

Engagement

Individual Engagement:

- The investor’s internal staff using shareholder power to influence corporate behavior, including through direct corporate engagement (i.e., communicating with senior management and company boards) and filing shareholder proposals.

Collaborative:

- The conduct of corporate engagement, as defined above; however, it is undertaken jointly with other investors.

Internal voting:

- The use of proxy voting guided by ESG guidelines where the voting decisions are undertaken internally and not outsourced to an external service provider.

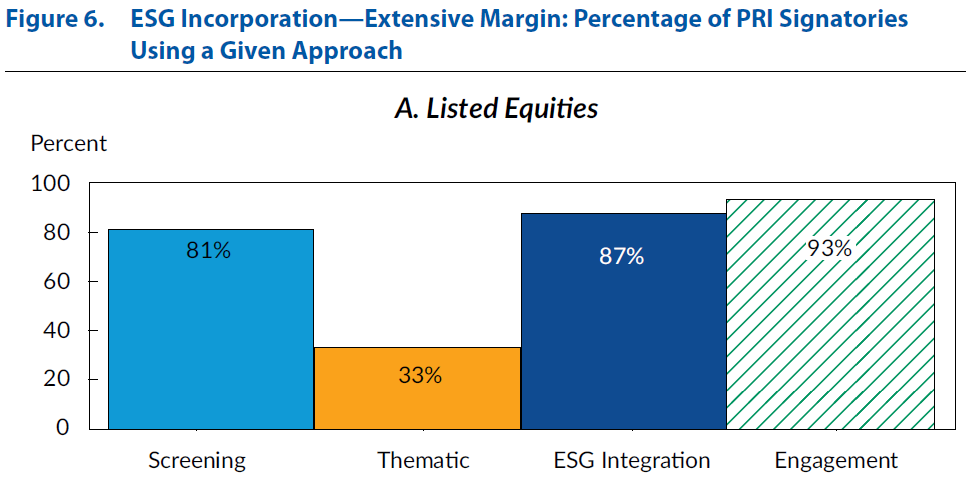

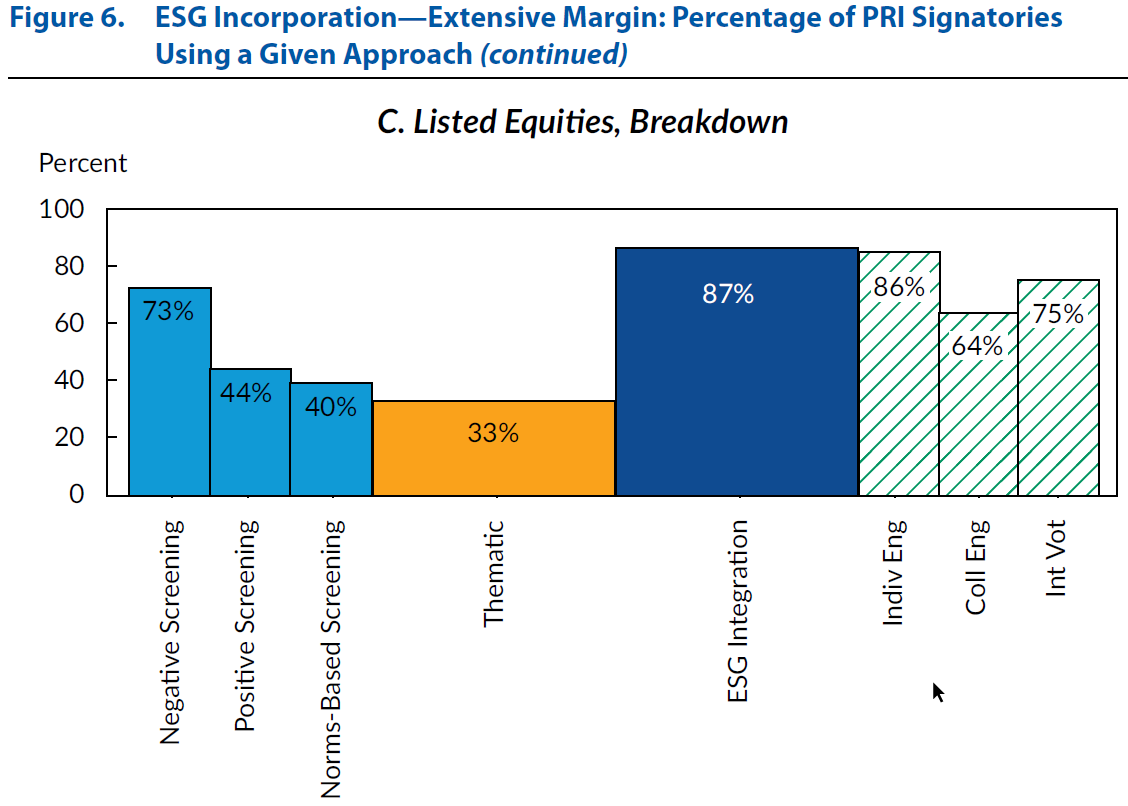

PRI

PRI

Among PRI signatories, almost all use Engagement.

PRI

Among PRI signatories, almost all use Engagement.

Question

Do you think that not investing in poor-ESG companies is enough?

My view.

It is not. Remember that a company can always find money elsewhere as long as there is enough capital available in the market and the company is profitable.

Question

Divestment is typically seen as a last resort. Some studies point to the considerable financial costs—for example, in fossil fuel divestment (Bessembinder 2016)—but some large institutional investors are nonetheless divesting what are viewed as unsustainable assets.

Others argue that if some institutional investors sell their shares, there will be willing buyers, thus diminishing the voice and impact of responsible institutional investors.

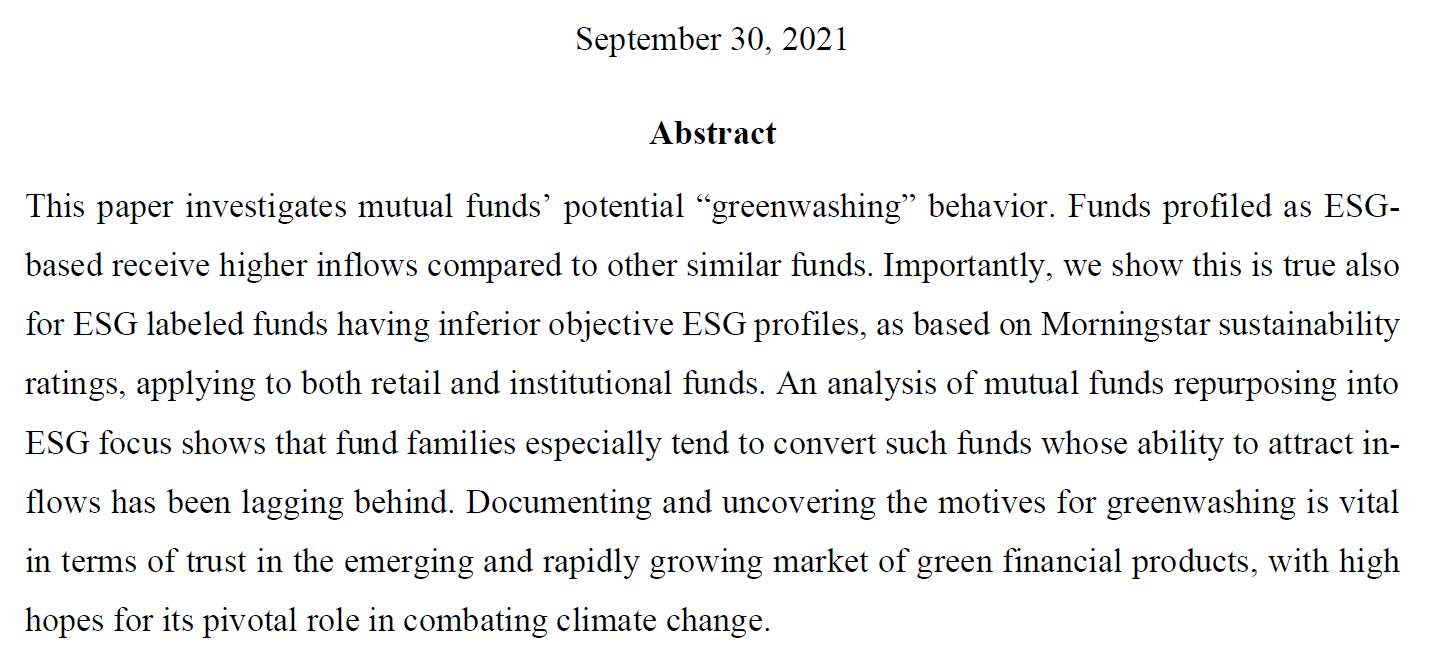

Greenwashing in mutual funds link

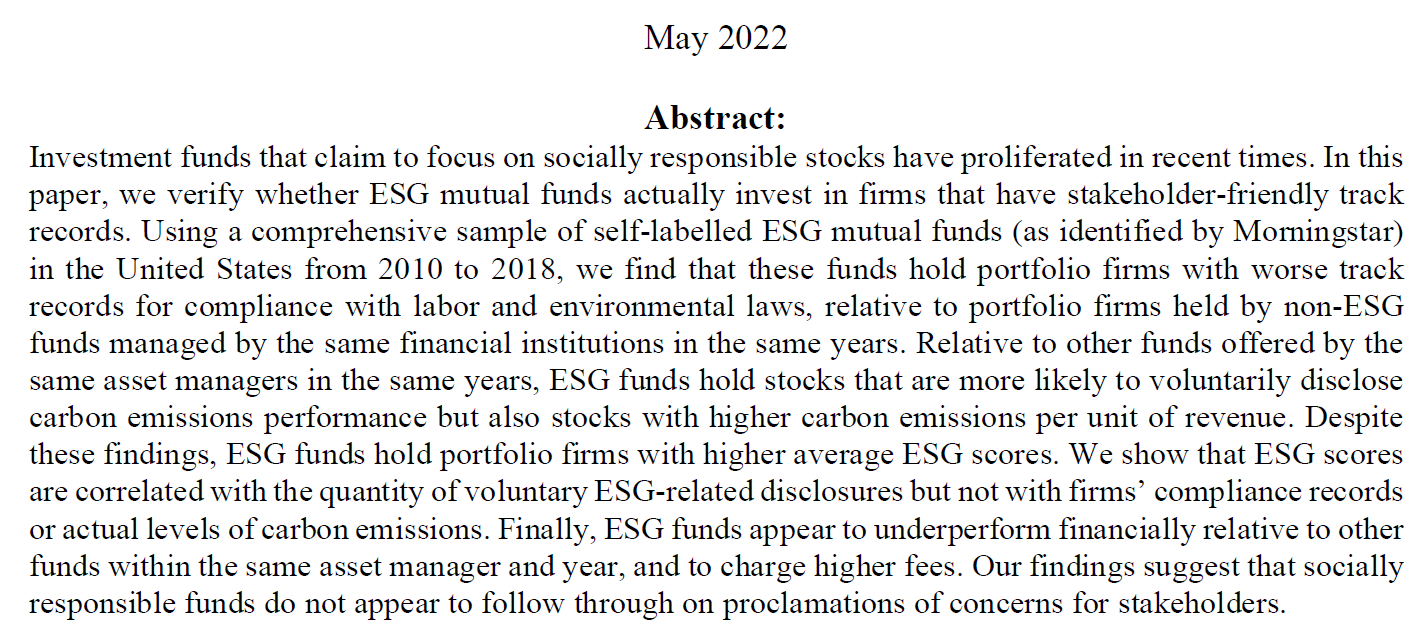

Do ESG Funds Make Stakeholder-Friendly Investments? link

Paris Agreement

The Paris Aligned Investment Initiative is a collaborative investor-led global forum enabling investors to align their portfolios and activities to the goals of the Paris Agreement.

The goal is to keep global warming to

Below 2C

Preferably, below 1.5C

Compared to pre-industrial levels.

The Paris Agreement sets out a global framework to avoid dangerous climate change by limiting global warming to well below 2°C and pursuing efforts to limit it to 1.5°C. It also aims to strengthen countries’ ability to deal with the impacts of climate change and support them in their efforts.

Where do these figures come from?

They seem easy to communicate but they are quite arbitrary,

Paris Agreement

Governments agreed link

on the need for global emissions to peak as soon as possible, recognising that this will take longer for developing countries;

to undertake rapid reductions thereafter in accordance with the best available science, so as to achieve a balance between emissions and removals in the second half of the century.

As a contribution to the objectives of the agreement, countries have submitted comprehensive national climate action plans (nationally determined contributions, NDCs). These are not yet enough to reach the agreed temperature objectives, but the agreement traces the way to further action.

Most Countries signed (192 + EU) source.

Trump’s withdraw in late 2020

Biden said he will rejoin

Paris Agreement

The Paris Aligned Investment Initiative (PAII) was established in May 2019 by the Institutional Investors Group on Climate Change (IIGCC).

As of March 2021, the initiative has grown into a global collaboration supported by four regional investor networks – AIGCC (Asia), Ceres (North America), IIGCC (Europe) and IGCC (Australasia).

118 investors representing $34 trillion in assets have engaged in the development of the Net Zero Investment Framework through the Paris Aligned Investment Initiative.

Paris Agreement

The international investor-led forum has four key areas:

Driving net zero investing commitments

Providing oversight of Paris Aligned Asset Owners’ disclosures and reporting.

Collaborating globally to update, identify or develop and further practical methodologies and approaches to enable Paris aligned investments

Supporting investors to implement commitments, using the Net Zero Investment Framework.

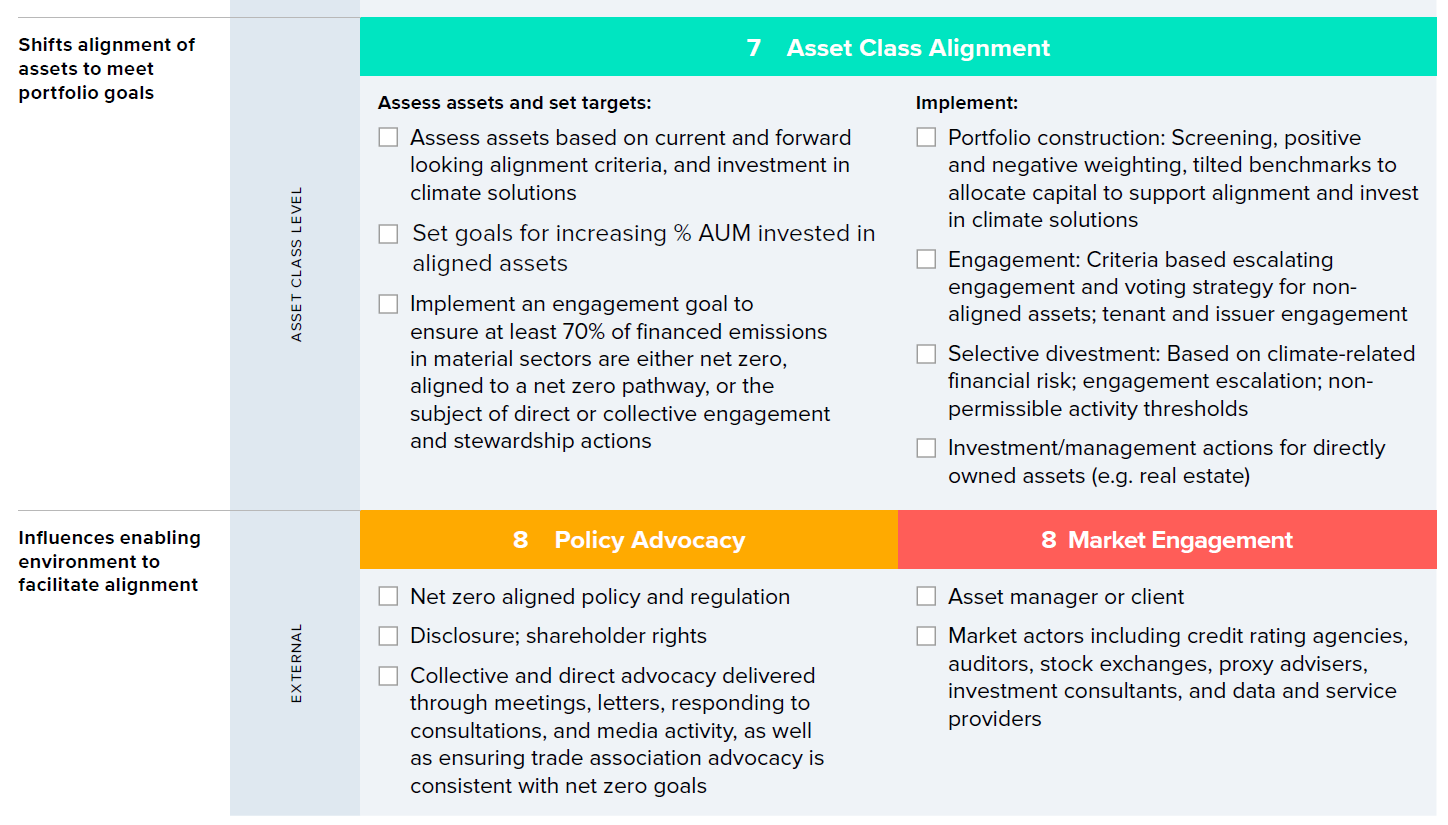

The Net Zero Investment Framework

The Net Zero Investment Framework

The Net Zero Investment Framework proposes key components of a net zero investment strategy. Such a strategy should focus on achieving two alignment objectives:

Decarbonise investment portfolios in a way that is consistent with achieving global net zero greenhouse gas (GHG) emissions by 2050.

Increase investment in the range of ‘climate solutions’ needed to meet that goal.

The Framework recognizes that investors have a range of levers at their disposal to drive carbonation and increase investment in climate solutions…

.. and these should be used to ensure progress in the real economy as well as reaching targets for the portfolio itself.

The Net Zero Investment Framework

The Net Zero Investment Framework

Cop 26

Glasgow, Nov 1- 12, 2021

Last conference that we’ve seen on climate change.

It is a direct continuation of Paris Agreement

200 countries participated and signed the accords

One key theme: fossil fuels

At the end of the conference, the accords were supposed to argue for the “full phase out of the use of fossil fuels”.

In the last minute, due to the influence of China and India, they changed the test for “phase down of the use of fossil fuels and ending subsidies on inefficient fossil fuel”.

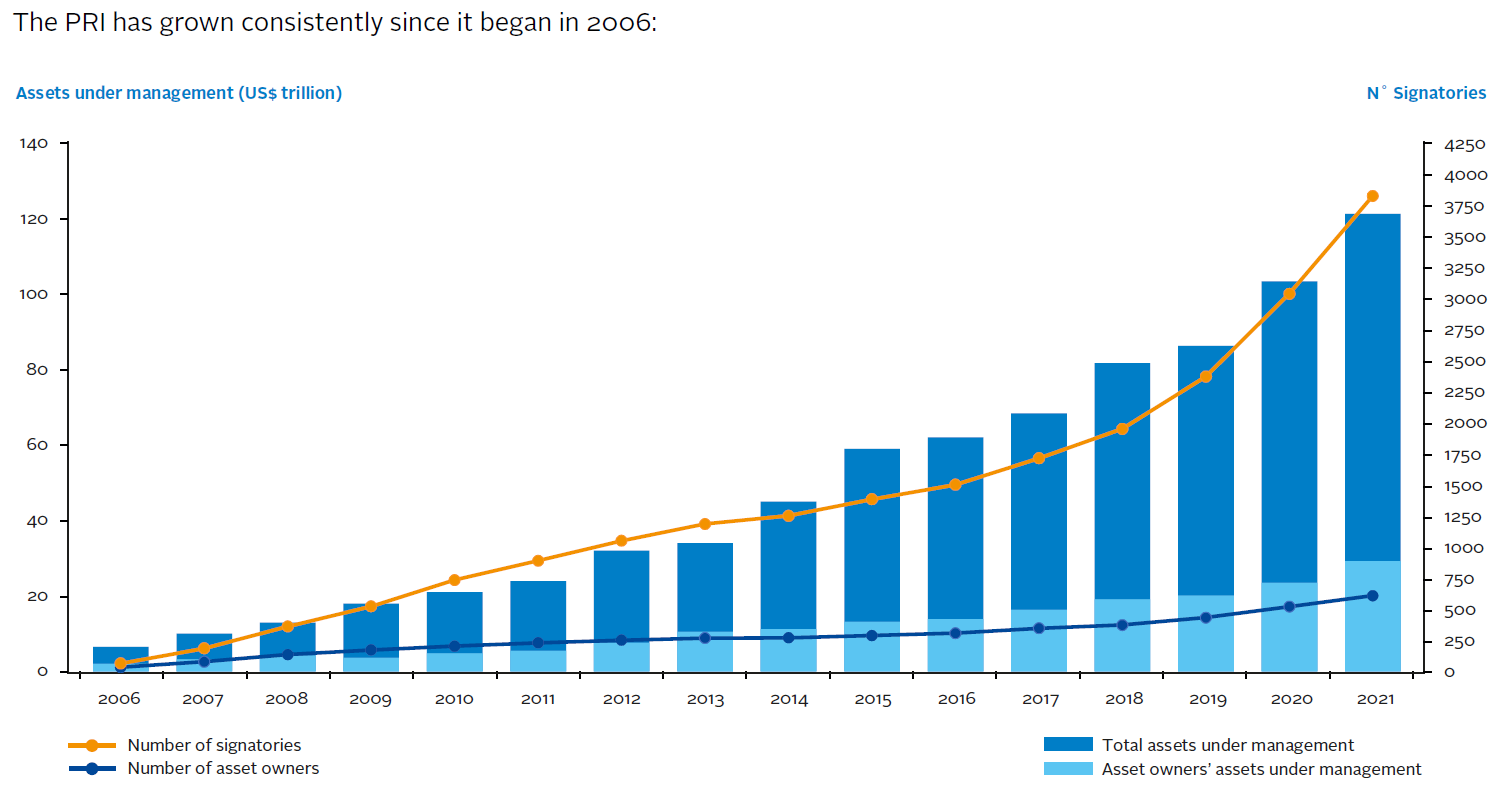

PRI

The UN PRI Principles

It is the most influential organization devoted to the advancement of ESG investing globally (Matos 2020).

About the PRI and the Six Principles

The PRI works with its international network of signatories to put the six Principles for Responsible Investment into practice.

Its goals are to understand the investment implications of environmental, social and governance issues and to support signatories in integrating these issues into investment and ownership decisions.

The six Principles were developed by investors and are supported by the UN.

They have more than 4,000 signatories from over 60 countries representing over US$120 trillion of assets.

The UN PRI Principles

In early 2005, the then United Nations Secretary-General Kofi Annan invited a group of the world’s largest institutional investors to join a process to develop the Principles for Responsible Investment.

A 20-person investor group drawn from institutions in 12 countries was supported by a 70-person group of experts from the investment industry, intergovernmental organisations and civil society.

PRI’s Mission

We believe that an economically efficient, sustainable global financial system is a necessity for long-term value creation. Such a system will reward long-term, responsible investment and benefit the environment and society as a whole.

As institutional investors, we have a duty to act in the best long-term interests of our beneficiaries. In this fiduciary role, we believe that environmental, social, and corporate governance (ESG) issues can affect the performance of investment portfolios (to varying degrees across companies, sectors, regions, asset classes and through time). We also recognise that applying these Principles may better align investors with broader objectives of society.

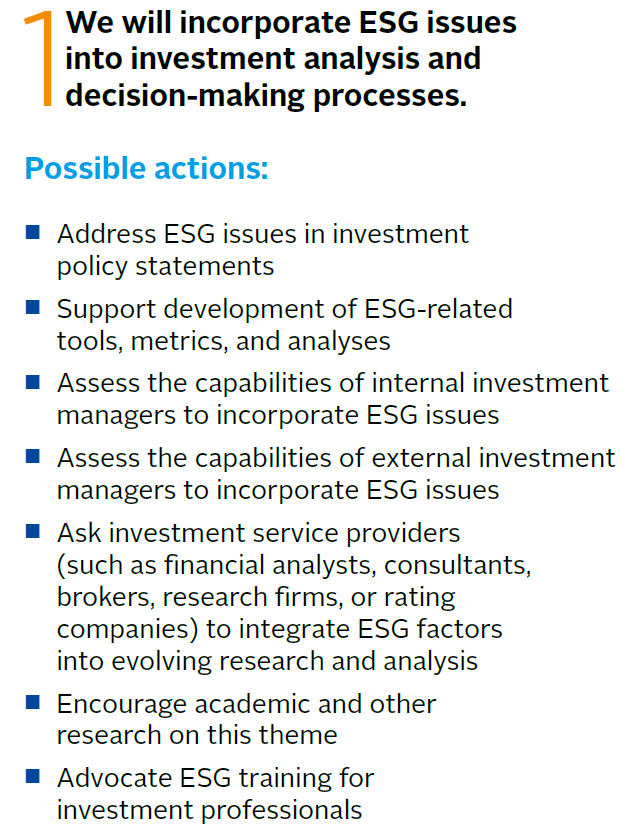

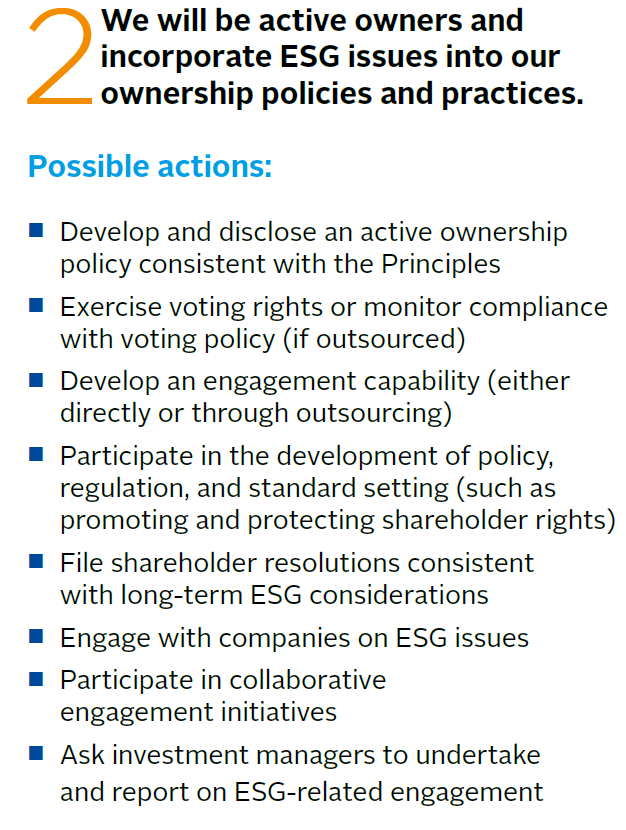

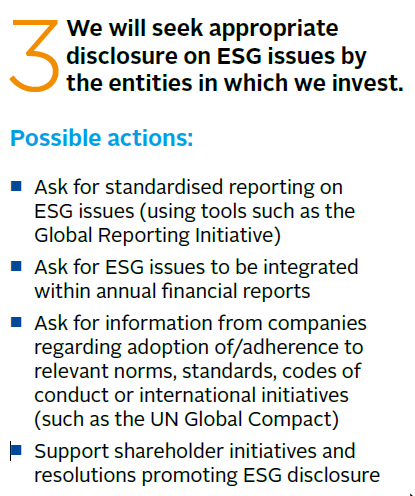

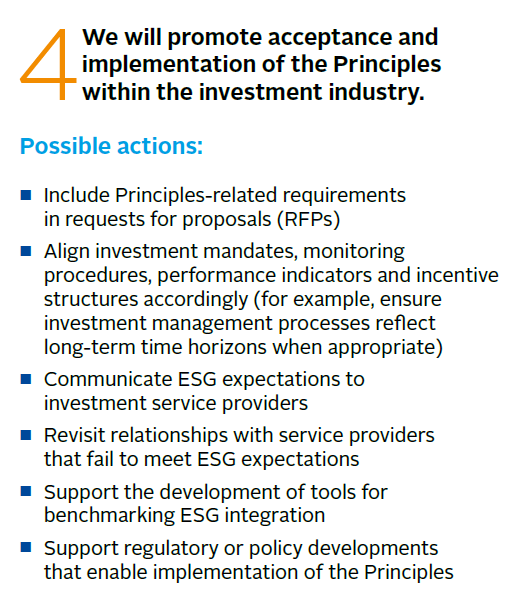

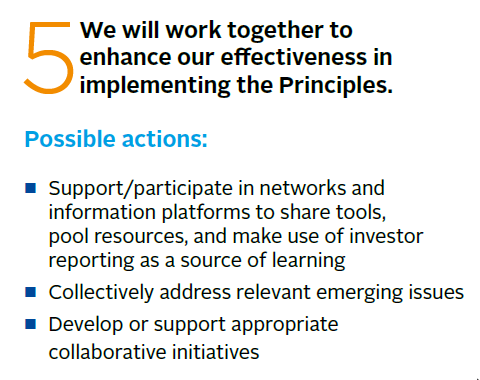

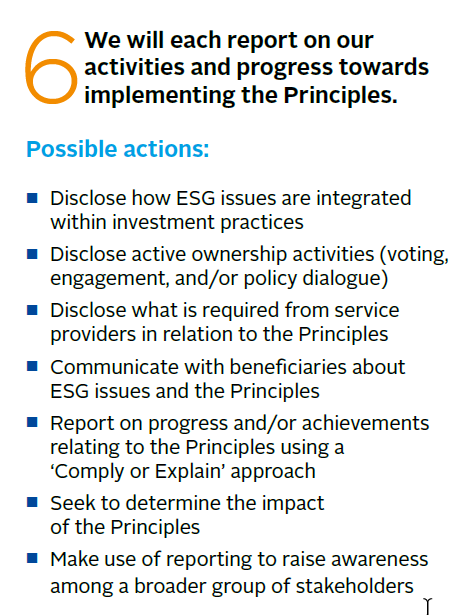

The UN PRI Principles (Source)

The UN PRI Principles (Source)

The UN PRI Principles (Source)

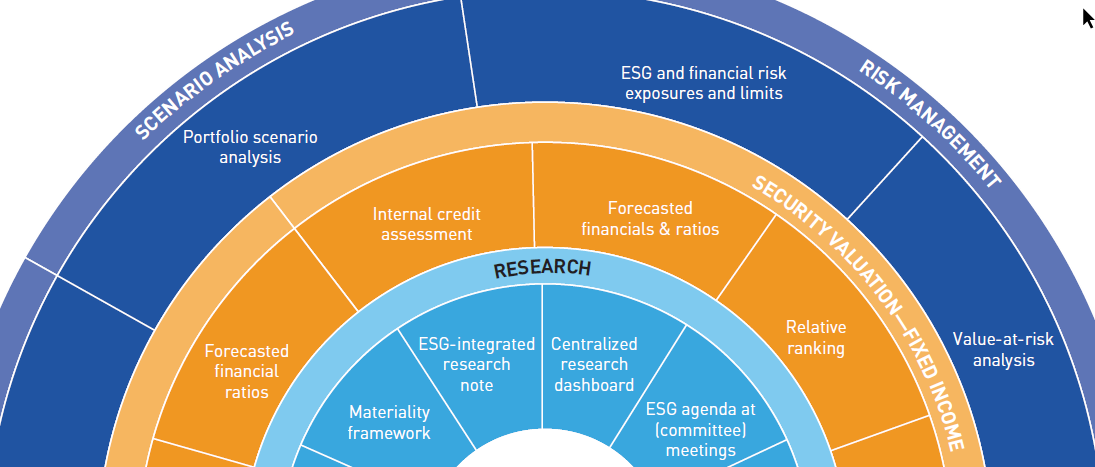

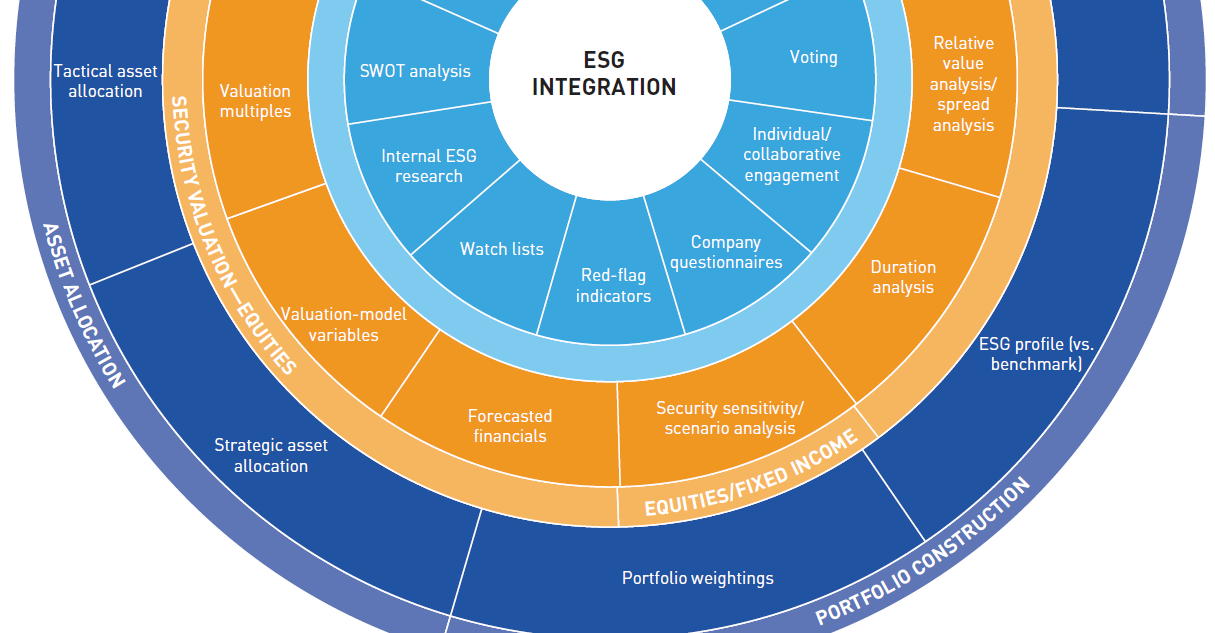

THE ESG INTEGRATION FRAMEWORK (link)

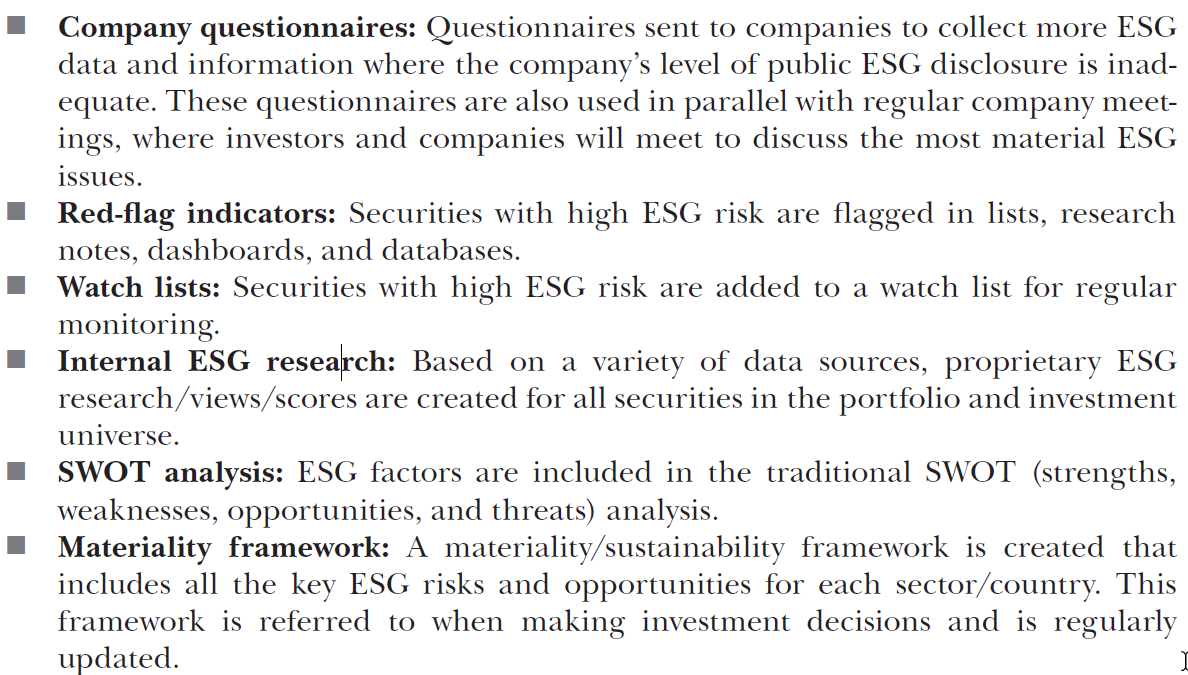

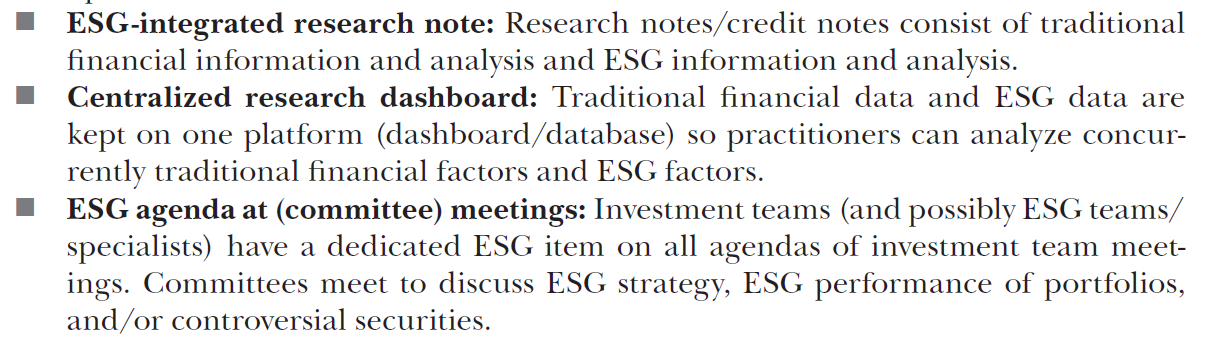

Qualitative Analysis

Qualitative Analysis

Qualitative Analysis

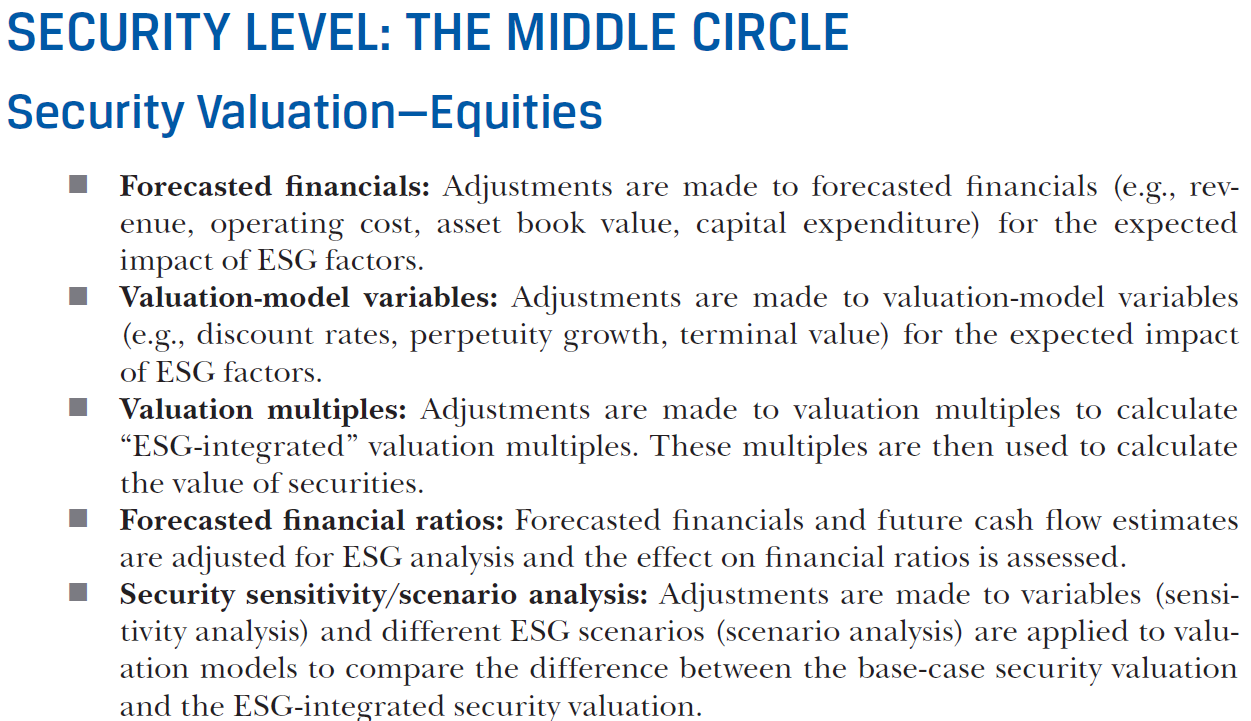

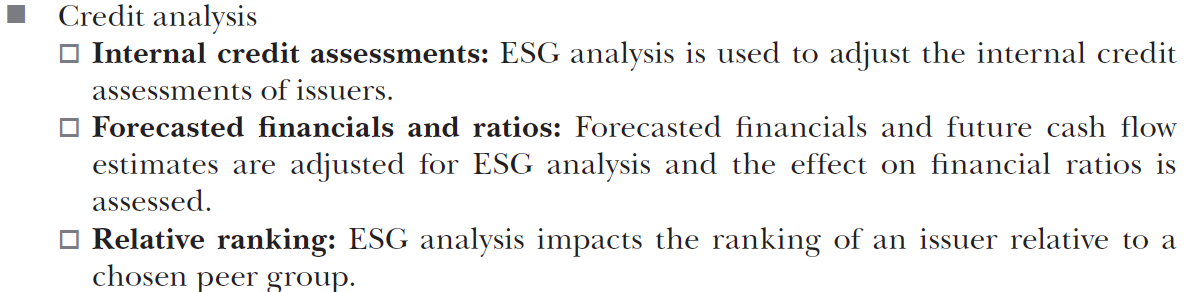

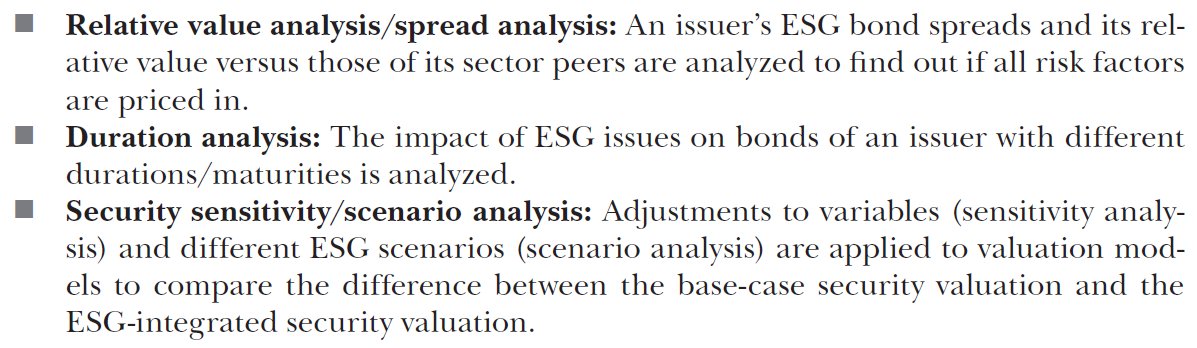

Security Valuation—Fixed Income

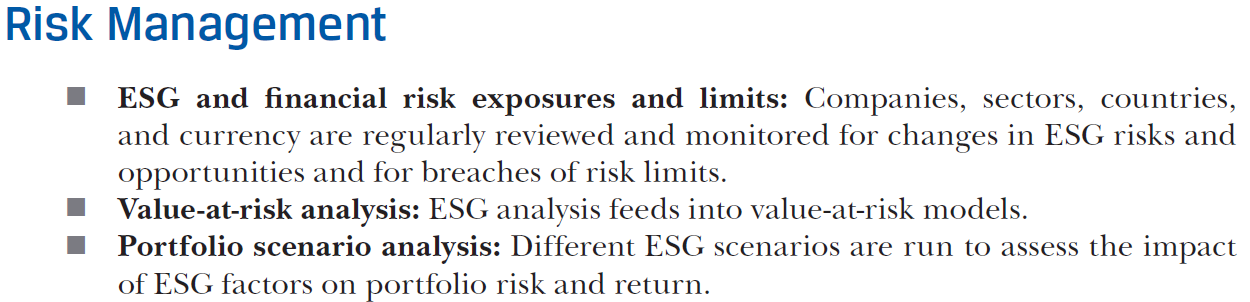

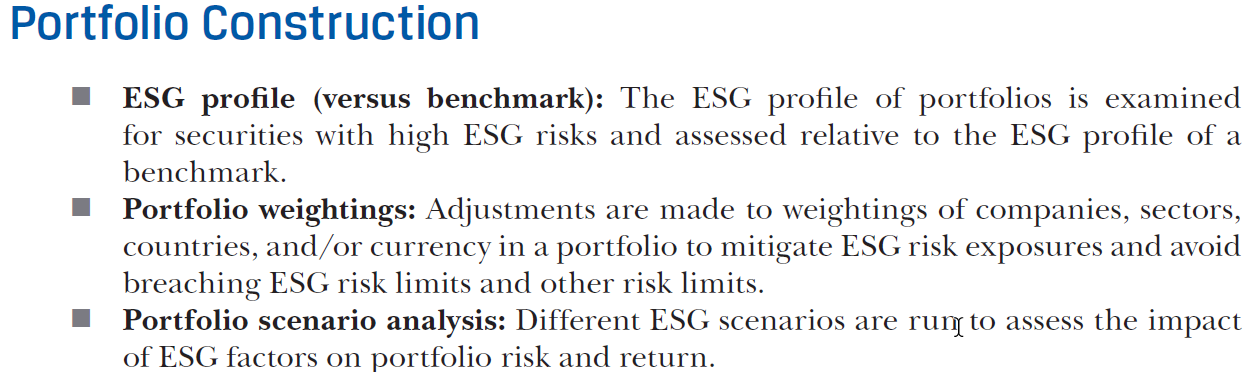

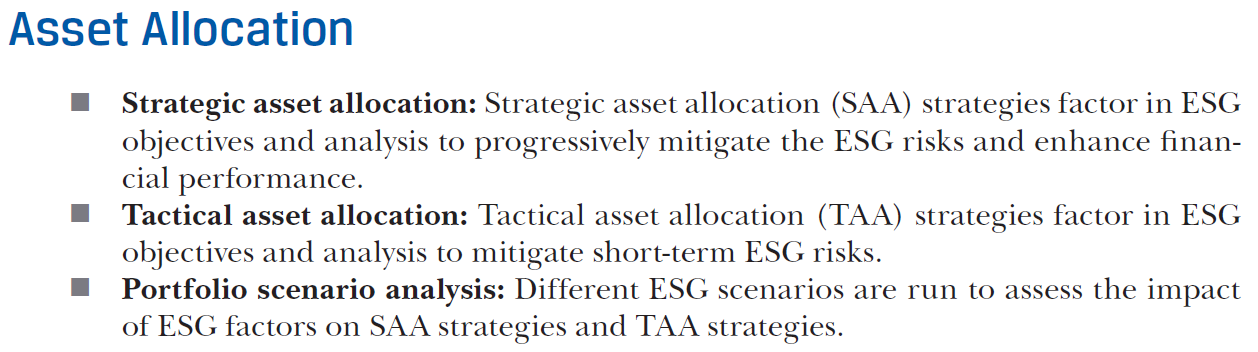

PORTFOLIO LEVEL: THE OUTER CIRCLE

PORTFOLIO LEVEL: THE OUTER CIRCLE

PORTFOLIO LEVEL: THE OUTER CIRCLE

Source

I hope you like this class!

Find me at:

https://eaesp.fgv.br/en/people/henrique-castro-martins

https://www.linkedin.com/in/henriquecastror/